PCB industry overview and development prospects analysis

Views: 1435Author: Site EditorPublish Time: 2023-05-26Origin: Site

PCB industry development so far, the application area involves almost all electronic products, mainly including communications, aerospace, industrial control medical, consumer electronics, automotive electronics and other industries. PCB industry growth and the momentum of the downstream electronic information industry are closely related, the two promote each other.

Specifically, network communications, computers, and consumer electronics have become the three main application areas of PCB, thanks to the development of 5G communication technology and the development trend of new energy vehicles, automotive intelligence, and automotive electronics have become one of the most rapidly growing PCB applications. With the continued development of the electronic information industry in the future, the application areas of PCB will become more and more extensive.

(1) The industry's main products and PCB product structure overview

According to the requirements of different electronic equipment, from the perspective of the number of layers and technical characteristics of PCB can be divided into single-sided, double-sided, conventional multilayer boards, flexible boards, HDI (High-Density Interconnect) boards, IC packaging substrates, and other six major product segments.

The end demand classification of printed circuit boards can be divided into enterprise-level user demand and individual consumer demand. Among them, enterprise-level user demand is mainly focused on communications equipment, industrial control, and medical and aerospace fields, PCB products often have high reliability, long service life, traceability, and other characteristics, the corresponding PCB enterprise qualification certification is more stringent, and certification cycle longer, individual consumer demand is mainly focused on computers, mobile terminals and consumer electronics and other fields, PCB products usually have Thin, small, bendable and other characteristics of the terminal demand.

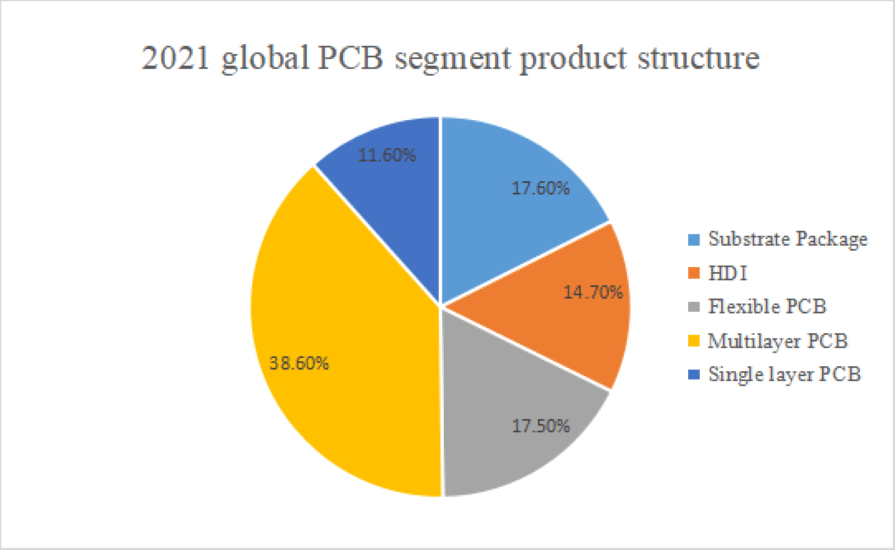

From a global perspective, according to Prismark's data, the current multilayer board still occupies a mainstream position in the PCB market, with the rapid development of electronic circuit industry technology, the integration of a wide range of components, electronic products for PCB high-density requirements more prominent, multilayer boards, HDI boards, flexible boards, and packaging substrates and other high-end PCB products gradually occupy a more important position in the market. From the perspective of each product category, in 2021, the global multilayer board and HDI board output value of $31.053 billion and $11.811 billion, respectively, of which, 8-16 layers of multilayer board growth rate is faster, reaching 29.80%, more than 18 layers of high multilayer board growth rate of 20.70%, HDI board growth rate of 19.60%.

From the domestic point of view, although there are still fewer domestic manufacturers who can produce high-technology products such as high multilayer boards, HDI boards, and packaging substrates, the proportion of such products is increasing year by year. In addition, according to Prismark forecasts, the future of China's PCB industry output value growth rate of each segment is higher than the global average, especially the high technology PCB represented by high multilayer boards, HDI boards, flexible boards, and packaging substrates.

Packaging substrate, for example, from 2016 to 2020, China's packaging substrate output value compound annual growth rate of about 5.50%, while the global average is only 0.10% industry transfer trend is obvious.

(2) China's PCB industry import and export situation

In recent years, in the context of slowing global economic growth, China's PCB output value and the proportion of year-on-year increase from the perspective of product structure, China's exports are mainly low-end PCB products, while imports are mostly high multilayer boards, HDI boards, flexible boards and packaging substrates and other high-end PCB products. However, with the increasing strength of China's PCB enterprises, the product structure of the import and export of the PCB industry has been gradually changing.

(3) PCB industry distribution

In the past decade, the Americas, Europe, and Japan's PCB production value in the global share of declining, while the global share of PCB production value in mainland China is rising, according to Prismark and the China Institute of Industrial Research, PCB production value in mainland China in 2021 accounted for 54.63% of the global output value, an increase of 0.40 percentage points over the previous year. In addition, in addition to mainland China, in other regions in Asia PCB production value of the global share is also slowly increasing. Global PCB industry production capacity (especially high multilayer boards, flexible boards, packaging substrates, and other high-tech PCB) gradually to mainland China as the representative of the Asian region concentration.

At present, China has formed a PCB industry in the Pearl River Delta region, the Yangtze River Delta region as the core area of the PCB industry gathering belt. In recent years, with the rise of labor costs in coastal areas, some PCB enterprises began to relocate their production capacity to central and western cities with better infrastructure conditions, such as Huangshi in Hubei, Guangde in Anhui, Suining in Sichuan and other places. The Pearl River Delta and Yangtze River Delta regions are expected to maintain a leading position in the PCB industry and continue to develop toward high-end and high-value-added products due to the advantages of talent, economic advantages, and industry chain support. In addition, the central and western regions will gradually become an important industrial base for China's PCB industry due to the inward migration of PCB enterprises.